10 mins

Data Center Colocation Trends 2026: Power, AI Density, and the New Rules of Colocation

The question buyers asked in 2022 was "do you have space?" The question in 2026 is "can you deliver power, and when?" Increasing demand from AI, cloud, and enterprise workloads has pushed North American colocation vacancy to a record low of 1%, with 92% of capacity currently under construction already precommitted before a single cabinet is installed. (JLL, 2026) Enterprises that once planned infrastructure 6 to 12 months ahead are now securing capacity 18 to 24 months before deployment.

In 2026, the data center colocation market is being reshaped by six converging forces: power scarcity, AI-driven density requirements, modular construction timelines, interconnection depth, edge computing demand, and enterprise cloud repatriation. Each one is rewriting which markets, which colocation data centers, and which digital infrastructure contract structures win.

Power has become the new real estate. With vacancy effectively at 0%, virtually all absorption is the result of preleasing with delivery times extending beyond 12 months.

Top 6 Data Center Colocation Trends in 2026

The top 6 data center colocation trends in 2026 are: power scarcity, AI-driven density requirements, modular construction timelines, interconnection depth, edge computing demand, and enterprise cloud repatriation.

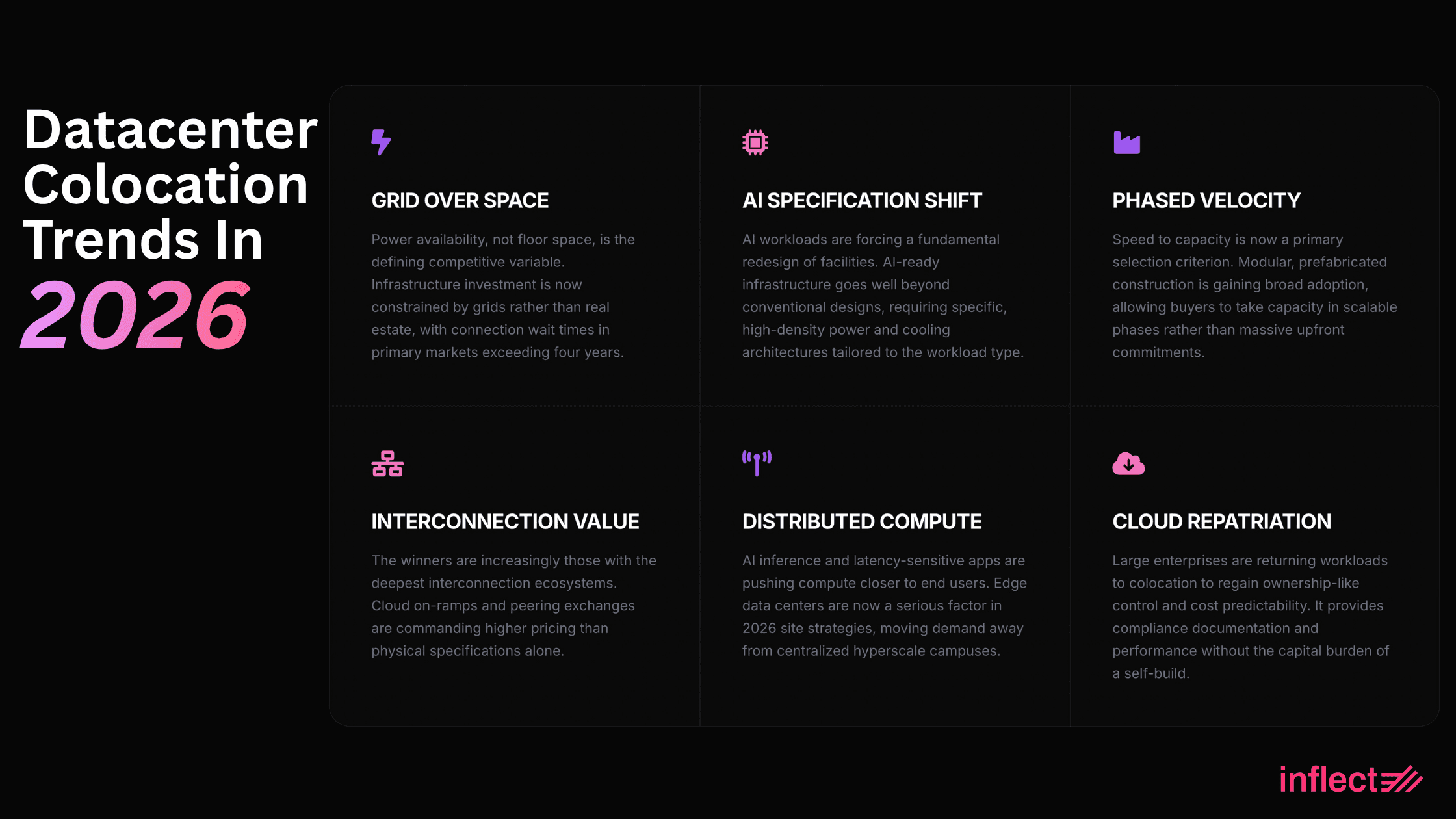

Trend 1: Power Has Overtaken Space as the Primary Market Constraint

Power availability, not floor space, is the defining competitive variable for the global data center colocation market in 2026. Data center infrastructure investment is now constrained by power grids rather than real estate, with average grid-connection wait times in primary markets exceeding four years and developers chasing power-advantaged regions over traditional urban proximity.

Global data center power consumption is projected to reach 1,050 TWh by 2026, a figure that illustrates how fundamentally the data center industry has been reshaped by GPU-intensive AI workloads, which draw significantly more electrical power per rack than conventional server deployments. (International Energy Agency, 2026)

More than 35 GW of data center capacity is under construction in North America alone, roughly equivalent to the UK's annual electricity consumption, with 92% of it already precommitted.

Colocation pricing for 250 to 500 kW deployments reached $184 per kilowatt per month in H1 2025, with requirements above 10 MW seeing increases of up to 19% in the same period. (CBRE, 2025)

Speed to power is now the primary site-selection criterion ahead of proximity, land cost, and data center construction cost. Northern Virginia, once the default US colocation hub, now faces substation queues pushing developers into West Texas, Louisiana, Ohio, Nebraska, and Iowa, markets that win on power availability, not prestige.

Renewable energy integration and energy efficiency improvements are accelerating in parallel, with operators pursuing solar, wind, and behind-the-meter generation to reduce exposure to strained power grids, cut long-term costs, and meet sustainability commitments.

For buyers: if a provider cannot confirm a substation status and energization date, they do not have usable capacity. Pipeline projections are not the same as committed power.

Trend 2: AI Workloads Are Rewriting Facility Specifications

AI-driven workloads are forcing a fundamental redesign of colocation facilities in 2026 and creating a new class of AI data centers built specifically for these requirements. AI-ready data center infrastructure goes well beyond what conventional data centers were designed to support, with specific requirements varying significantly by workload type.

AI training clusters, which run large-scale model development jobs, typically require 30 to 100 kW per rack or higher and place the most extreme demands on power distribution, cooling infrastructure, and floor loading.

AI inference workloads, which serve real-time AI responses to end users, are more broadly deployable. Many inference deployments run comfortably at 10 to 20 kW per rack, making them accessible in a wider range of colocation environments, though latency and geographic distribution requirements become critical selection factors.

At higher densities, air cooling becomes inadequate and power and cooling must be redesigned together. Liquid cooling, including rear-door heat exchangers, direct-to-chip systems, and immersion cooling, transitions from a premium option to a core cooling infrastructure requirement for dense AI deployments.

Inference workloads are growing fastest and require higher availability, geographic distribution, and tighter latency guarantees than centralized training clusters. Some experts even anticipate inference overtaking training as the dominant AI requirement by 2027.

The global AI market is forecast to reach $1.81 trillion by 2030 at a 36.6% CAGR, driven by the rapid growth of AI models across enterprise, fintech, and consumer applications, making AI infrastructure investment one of the most durable demand drivers the colocation sector has seen. (Grand View Research, 2025)

For buyers: assess your specific workload before evaluating AI-readiness. A provider that supports 15 kW per cabinet with rear-door cooling may be the right fit for inference; a training cluster requires a materially different facility conversation.

Trend 3: Modular and Phased Delivery Are Now a Competitive Requirement

Speed to capacity has become a primary selection criterion in 2026, and modular or prefabricated construction of new data centers is gaining broad adoption because it delivers scalable infrastructure and scalable colocation options faster than conventional builds, while allowing buyers to take capacity in phases rather than committing upfront.

Traditional data center construction runs 18 to 24 months from groundbreaking to commissioned capacity, before factoring in power delivery delays. Prefabricated modular data centers compress physical construction to 4 to 6 months by completing build and test work in factory conditions before shipping to site.

AI infrastructure supply chains are adding further volatility to project timelines: memory vendors are prioritizing HBM production, and longer lead times for advanced substrates, optics, and high-speed networking components are compounding schedule risk. Phased deployment reduces exposure by minimizing the upfront commitment.

Market research firms consistently show strong growth in modular data centers, with Grand View Research projecting the market to rise from US$29.04 billion in 2024 to US$75.77 billion by 2030 and MarketsandMarkets projecting US$29.93 billion to US$79.49 billion over the same period.

For buyers: ask whether available capacity is in a modular or conventionally constructed hall, what phased expansion looks like within your contract term, and what the lead time is from signature to a powered, networked cabinet.

Recommend Reading: Total Cost of Ownership for Modular Data Centers vs. Traditional Builds

Trend 4: Interconnection Depth Is the Key Differentiator

The colocation provider that wins in 2026 is increasingly the one with the deepest interconnection services ecosystem. Cloud computing on-ramps, carrier-neutral access, peering exchanges, and financial network cross-connects are commanding higher occupancy and pricing than physical specifications alone, because buyers are colocating near the ecosystems their workloads depend on, not just buying rack space.

A workload requiring simultaneous low-latency access to AWS, Microsoft Azure, and Google Cloud can achieve single-digit millisecond round-trip times through direct connectivity and low latency infrastructure at a carrier-neutral facility with cloud services on-ramps already in the building. The same workload connecting over the public internet from a facility without direct interconnection adds 20 to 40 milliseconds per round trip and introduces routing variability that compounds under load.

Interconnection services compound over time. A facility with diverse carrier terminations and multiple cloud on-ramps attracts tenants whose value grows as the ecosystem expands, which attracts more tenants, deepening the ecosystem further. The facilities that built this fabric early are structurally advantaged over facilities trying to build it now.

For financial and trading workloads, latency differences are measurable in execution quality. For latency-sensitive enterprise applications, they show up in user experience. Low latency infrastructure is increasingly the decisive factor in facility selection.

For buyers: get specific answers on how many carriers terminate in the facility, which cloud on-ramps are available and at what latency, and what cross-connect fees and provisioning timelines look like in writing.

Trend 5: Edge Computing Is Reshaping Where Capacity Gets Built

Edge data centers and distributed infrastructure are a serious and growing factor in 2026 site strategy, as AI inference demand and latency-sensitive applications push compute requirements closer to end users and away from centralized hyperscale campuses.

Inference workloads for AI services, industrial automation, telemedicine, and real-time analytics all have latency requirements that centralized colocation cannot fully satisfy at distance. Edge deployments position compute within milliseconds of where data is consumed.

The same power grid constraints driving development to secondary markets are also opening space for edge data centers in geographies that were previously overlooked. Markets with strong local power availability and growing digital demand are increasingly viable edge colocation sites.

For enterprises, edge computing and colocation are complementary rather than competing strategies: centralized colocation handles core production and regulated workloads with full network infrastructure and IT infrastructure support, while edge nodes handle latency-sensitive processing closer to users or devices.

For buyers: edge deployments are not a replacement for primary colocation strategy. They are an extension of it. Evaluate providers that can support both centralized and edge capacity within a consistent contract and operations model.

Trend 6: Enterprise Repatriation Is Reinforcing Colocation Demand

Large enterprises undertaking enterprise digitalization are returning workloads from cloud providers to colocation services in 2026, not to on-premises infrastructure, but to colocation, which provides ownership-like control, cost predictability, and compliance documentation without the capital commitment of a self-build.

Hyperscale operators account for 44% of global data center capacity today and are expected to reach 61% by 2030, reflecting continued growth in cloud and AI-driven workloads and a shift toward owned and build-to-suit facilities. (SRG Research, 2025) That structural shift leaves a well-defined role for multi-tenant colocation: mission-critical workloads that need ownership-like control and compliance documentation.

Cost efficiency analysis consistently shows that stable, high-volume workloads run materially cheaper in colocation. Cloud cost optimization at scale routinely surfaces egress fees, reserved instance lock-in, and management overhead that erode the economics of keeping predictable workloads in public cloud.

Regulated industries find the compliance documentation chain simpler in colocation. The firm owns its hardware, controls data residency explicitly, and holds contractual access log deliverables. Equivalent compliance posture in cloud for workloads subject to SEC Rule 17a-4, HIPAA, or PCI DSS requires additional architectural effort that colocation eliminates by design.

The result is not colocation replacing cloud but mature hybrid cloud strategies that optimize for operational efficiency across the full workload portfolio: cloud for development, analytics, and variable demand; colocation for production, regulated, and latency-sensitive applications where control and compliance matter most.

What Colocation Buyers Are Prioritizing in 2026

Colocation buyers across enterprise, AI infrastructure, fintech, and cloud-adjacent deployments are evaluating providers in 2026 across six criteria that directly reflect the market conditions above.

Buyer Priority | What It Means in Practice |

|---|---|

Power certainty | Committed, deliverable MW with redundant power feeds, available now. Ask for the substation status and energization date. |

Density support | Cooling infrastructure and power distribution that matches your specific workload, whether inference at 10-20 kW or training at 50+ kW per cabinet. |

Time to capacity | Realistic timeline from contract to a powered, networked cabinet. For modular builds, the phasing schedule in writing. |

Interconnection | Carrier-neutral facility with direct cloud on-ramps, peering exchange access, and cross-connects to the networks your workloads depend on. |

Regional flexibility | Willingness to evaluate secondary and tertiary markets, including retail colocation options, where power delivery and pricing are more favorable than primary markets. |

Edge capability | Whether the provider can support edge nodes alongside enterprise-grade infrastructure for centralized workloads within a consistent contract and operations model. |

Data Center Colocation Market Prediction in 2026

The global data center sector is forecast to grow at a 14% CAGR through 2030, with roughly 100 GW of new digital infrastructure capacity coming online in that period. Rapid growth continues to outpace supply: global occupancy is approaching 97%, Americas rents are growing at 7% CAGR, and European vacancy is forecast to reach an all-time low of 6.5% by end 2026. Operational reliability is now a direct function of how well a provider has secured power, cooling, and interconnection before you sign. Eleven of the largest cloud providers spent roughly $450 billion on data center infrastructure in 2024, and experts project global capex to exceed $1.7 trillion by 2030.

This market does not normalize quickly. Buyers who treat 2026 as an anomalous tight period and wait for conditions to ease are likely to find those conditions persist well into their planning horizon. The consistent conclusion across all six trends: plan earlier, ask specific questions about power, and contract for phased expansion rights in your initial agreement rather than assuming space will be available when you need more of it.

How to Source Colocation, AI-Ready Infrastructure, and Wholesale Data Center Capacity in 2026

Inflect is a digital infrastructure marketplace and advisory platform where enterprises, AI startups, and hyperscale tenants can source, compare, and transact colocation capacity ranging from a single retail rack to wholesale data center deployments above 100 MW, with handpicked lists for AI-ready infrastructure, modular data center providers, and also filters on marketplace for liquid cooling, HPC-capable facilities, and interconnection ecosystems across primary, secondary, and tertiary markets globally.

The six trends covered in this post each map directly to sourcing problems that Inflect is built to solve:

Power certainty and site selection: Backing up by close collaboration with 1000+ data center colocation providers globally with APIs and data integrated, Inflect is able to help source specific capacity in certain regions or markets.

AI-ready infrastructure: Filter colocation providers on Inflect marketplace by power density per cabinet, cooling architecture and more. Whether you are deploying an AI inference workload at 15 kW per rack or a GPU training cluster above 50 kW, Inflect narrows the provider set to facilities that can actually support your workload type.

Wholesale colocation above 100 MW: Inflect connects large-scale tenants directly with wholesale colocation providers and campus operators globally, including power-advantaged secondary and tertiary markets where new capacity is coming online faster than constrained primary hubs.

Modular and phased delivery: Inflect's provider network includes modular data center operators whose prefabricated builds commission capacity in 4 to 6 months rather than 18 to 24 months, with phased expansion options structured into contracts from day one.

Interconnection and cloud on-ramps: Filter facilities by carrier count, cloud on-ramp availability for AWS, Microsoft Azure, and Google Cloud, peering exchange access, and cross-connect fees. Interconnection depth is searchable and comparable, not buried in a separate sales conversation.

Edge and distributed infrastructure: Source edge data centers for latency-sensitive AI inference, industrial automation, and real-time analytics deployments alongside centralized colocation for core production environments, within a single sourcing workflow.

Inflect also provides 0-Cost advisory services for organizations navigating the 2026 market for the first time or renegotiating existing colocation agreements. The advisory team covers RFP development, provider evaluation, contract negotiation, and long-term capacity planning across retail colocation, wholesale colocation, and hybrid cloud infrastructure strategies.

Find Colocation Capacity That Matches 2026 Market Realities

Compare providers across power availability, AI density support, interconnection depth, edge capability, and regional flexibility. Transparent pricing across primary, secondary, and tertiary US markets. Phased and modular capacity options with clear timelines from contract to commissioned cabinet.

Looking for huge capacity or specific infrastructure in specific markets?

About the Author

Chanyu Kuo

Director of Marketing at Inflect

Chanyu is a creative and data-driven marketing leader with over 10 years of experience, especially in the tech and cloud industry, helping businesses establish strong digital presence, drive growth, and stand out from the competition. Chanyu holds an MS in Marketing from the University of Strathclyde and specializes in effective content marketing, lead generation, and strategic digital growth in the digital infrastructure space.

Contact:

Email: